In a world where prices rise faster than salaries and financial responsibilities seem endless, saving money has become more important than ever. Whether you’re a student, a working professional, or someone building a family budget, smart saving habits can completely transform your financial future.

Saving money is not just about restricting yourself—it’s about making better choices that give you more freedom, security, and peace of mind. The good news? Anyone can learn to save wisely with a little planning and consistent effort.

Here’s a complete guide on how to save money intelligently and sustainably.

1. Start by Tracking Your Expenses

Before you try to save money, you need to know where your money actually goes. Most people underestimate their daily expenses—small purchases like snacks, subscriptions, or online shopping add up quickly.

How to Track Your Spending:

- Use apps like Walnut, Money Manager, or Mint.

- Maintain a simple Excel sheet or notebook.

- Review bank statements every month.

When you have a clear view of your spending habits, you can identify unnecessary expenses and areas where you can cut back.

Why it matters:

You cannot fix what you don’t measure. Tracking expenses is the first step toward financial awareness.

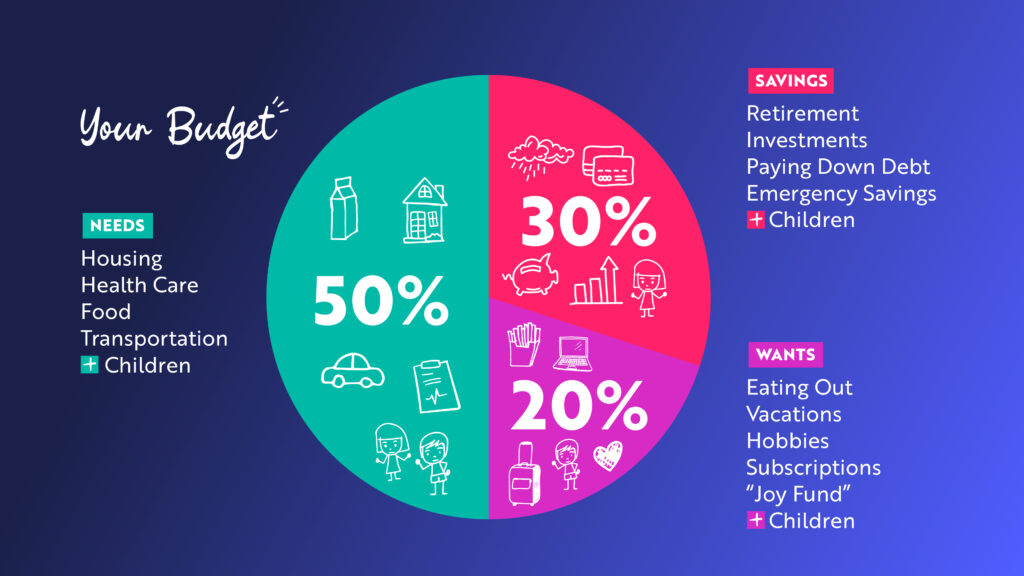

2. Build a Realistic Monthly Budget

A budget isn’t a restriction—it’s a plan. A good budget tells your money where to go instead of wondering where it went.

Create a Simple Budget Using the 50-30-20 Rule:

- 50% for needs (rent, groceries, bills)

- 30% for wants (shopping, dining, entertainment)

- 20% for savings and investments

If 20% seems too high initially, start with 10% and increase gradually. The goal is consistency, not perfection.

Tip: Automate your savings. Set up automatic transfers to your savings account or investment fund on salary day.

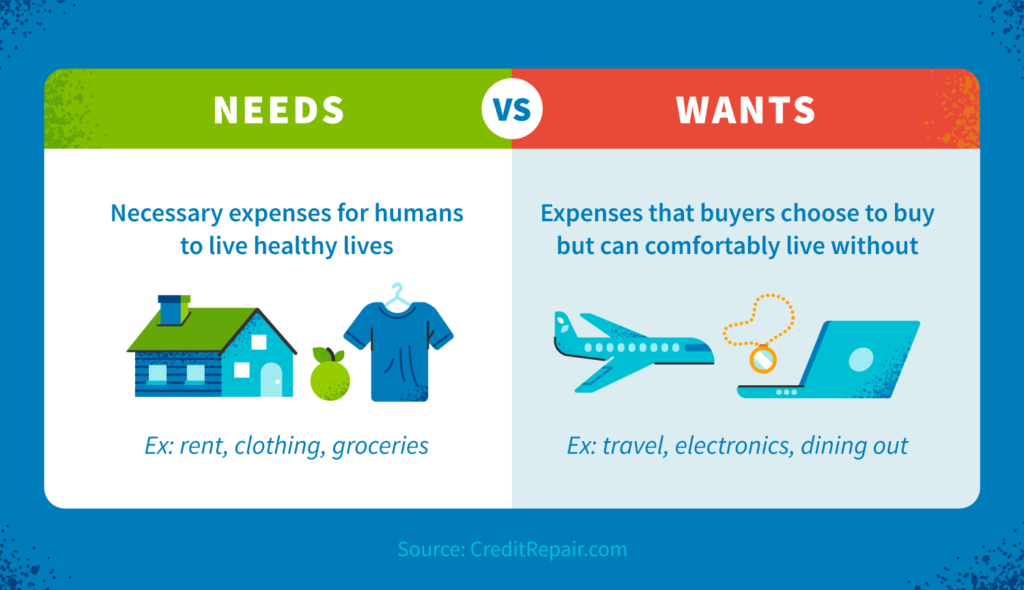

3. Distinguish Between Needs and Wants

This is one of the most powerful habits in saving wisely.

Needs are essential things:

- Food

- Housing

- Utilities

- Transport

- Medicines

Wants are extras:

- Eating out

- Premium subscriptions

- Fashion purchases

- Gadgets

- Impulse buys

Before buying anything, ask yourself:

“Do I really need this, or do I just want it?”

A simple pause often prevents unnecessary spending.

4. Cut Down on Debt and Avoid High-Interest Loans

Debt is one of the biggest obstacles to saving money. Credit cards and personal loans often come with high interest rates, which eat into your income.

Smart ways to manage debt:

- Pay high-interest loans first.

- Avoid “minimum balance” payments on credit cards.

- Refinance or consolidate loans if possible.

- Use credit cards responsibly—pay the full amount every month.

Reducing debt gives you room to save more and lowers financial stress.

5. Build an Emergency Fund

An emergency fund is money saved specifically for unexpected events like medical emergencies, job loss, urgent repairs, or travel. Without this fund, people end up using credit or borrowing money during crisis situations.

How much should you save?

Ideally, 3–6 months of essential expenses.

Start small—₹1,000 or ₹5,000 per month. Over time, it grows into a safety cushion that protects your financial stability.

\

6. Be a Smart Shopper

Saving money doesn’t mean you stop buying things. It means buying them wisely.

Smart shopping strategies:

- Compare prices before buying.

- Use discount coupons and cashback apps.

- Buy groceries in bulk when possible.

- Avoid impulse purchases—wait 24 hours before deciding.

- Take advantage of festive sales but only buy what you need.

A little patience and planning can cut your expenses significantly.

7. Invest Your Savings to Make Money Grow

Saving money is great—but growing money is even better. Simply keeping money in a savings bank account won’t beat inflation.

Smart investment options include:

- SIPs in mutual funds

- Fixed deposits

- Public Provident Fund (PPF)

- Index funds

- Stock market (only with proper knowledge)

- Gold (Sovereign Gold Bonds or ETFs)

Start early, even with small amounts—you’ll benefit from compounding over time.

8. Reduce Lifestyle Inflation

As income increases, people tend to increase their spending too—this is called lifestyle inflation. It kills savings.

How to avoid it:

- Maintain your current lifestyle even when your salary rises.

- Increase your savings percentage with every raise.

- Reward yourself occasionally, but don’t overdo it.

A simple lifestyle can lead to a wealthy future.

Final Thoughts: Saving Money Is a Skill, Not a Sacrifice

Saving money wisely does not mean living a boring or restricted life. It means taking control of your finances, securing your future, and giving yourself more freedom to enjoy life without stress.

Start small. Be consistent. Make saving a habit rather than an effort.

Your financial future is built by the decisions you make today. Begin now, and your future self will thank you.

Checkout More Content: